Content presented here focuses exclusively on legitimate financial planning education, aiming to improve understanding of concepts, methodologies, and analytical approaches without promoting any specific securities, strategies, or market participation decisions.

No Personalized Advice:

No personalized recommendations, solicitations, or assurances are provided, and no guarantees of future performance, outcomes, or returns are implied, expressed, or otherwise suggested under any circumstances within this educational material.

Data Limitations:

Uploaded results rely on deterministic, offline data because live data was unavailable within the sandbox environment, and therefore outputs should be interpreted as illustrative examples rather than real time analyses.

Long-Only Scope:

All research language used is long only, avoiding options, puts, short selling, or bearish strategies, ensuring the discussion remains focused on traditional asset ownership and positive directional exposure concepts overall.

Table Of Contents

Part 1: Opening Context And Article Focus Introduces the AMZN long-only timing problem, the article focus, and the business reason for creating evidence before debating any allocation decision. This part helps readers understand the trading voice, market context, and why the workflow is educational rather than advisory.

Part 2: Agentic Architecture And Governance Controls Explains the AgentCore and Strands operating model, including orchestrator, data agent, strategy agent, risk reviewer, governance checker, tool permissions, audit artifacts, and human approval boundaries. This part makes the architecture readable before the code and strategy records appear.

Part 3: Data, Benchmarks, And Backtest Harness Covers real or approved data inputs, benchmark context, OHLCV alignment, data lineage, and the reusable backtest harness. This part shows how AMZN, Nasdaq 100, S&P 500, and Dow Jones context become reviewable research evidence.

Part 4: Strategy Framework And Long-Only Code Logic Explains the implementation framework behind the article’s strategy family, including entry logic, exit logic, sizing, execution separation, risk controls, and plain-language code review. This part prepares readers to inspect the strategy examples without losing the governance context.

Part 5: Trade Ledger And Position Management Evidence Focuses on the trade ledger, position-management evidence, turnover, drawdown review, and why each simulated entry and exit must be traceable. This part turns the backtest from a chart into a reviewable sequence of decisions.

Part 6: Governance, Risk Review, And Institutional Challenge Collects institutional review guidance, model-risk questions, challenge workflow, audit trail expectations, production readiness, parameter sensitivity, failure modes, and committee evidence standards. This part improves readability by grouping governance content before the strategy records.

Part 7: Strategy Catalog And Reading Method Presents the strategy catalog and the method for reading strategy records. This part gives readers a short navigation bridge between governance concepts and the individual strategy examples.

Part 8: Strategy Records 1-5: EMA, Breakout, Donchian, RSI, And Bollinger Groups Strategies 1-5 into one readable part so readers can review the article’s five strategy records without turning every strategy into a separate top-level TOC item. The focus is research purpose, code logic, risk controls, and trade-ledger interpretation.

Part 9: Executive Committee Summary And Speaking Close Converts the technical research into executive and committee language. This part summarizes what was tested, what remains uncertain, why the workflow does not replace human accountability, and how to speak about results responsibly.

Part 10: Sources, Data Notes, And Final Disclosures Keeps sources, data notes, limitations, and final disclosure language together. This part clarifies data assumptions, time windows, AWS design references, and the educational boundary of the article.

Part 1: Opening Context And Article Focus

Related summary: Introduces the AMZN long-only timing problem, the article focus, and the business reason for creating evidence before debating any allocation decision. This part helps readers understand the trading voice, market context, and why the workflow is educational rather than advisory.

Opening And Market Context

Related summary: Establishes the Amazon long-only timing problem, explains why backtesting belongs in institutional review, and frames the article as evidence generation rather than prediction. The section connects a profitable AMZN position to risk discipline, benchmark awareness, disclosure language, and committee-ready communication.

A large unrealized Amazon gain can create confidence, but confidence is not a control framework. The institutional question is not only whether the long position worked historically. The better question is whether the desk can explain why exposure was added, why it was held, why it was reduced, and how the decision behaved relative to broad equity and technology regimes.

The former delivery guidance is now digested directly into the opening: use evidence language, show assumptions, and avoid certainty. A strong speaker does not open with a promise. A strong speaker opens with a research question, states the constraints, and tells the audience exactly what the backtest can and cannot prove.

Amazon is a single-name position, yet it is influenced by growth appetite, liquidity, rates, consumer expectations, cloud-computing sentiment, and broad equity risk. That is why the article uses Nasdaq 100, S&P 500, and Dow Jones Industrial Average as context rather than treating AMZN as an isolated line on a chart.

The purpose of the workflow is disciplined evidence creation. Bedrock AgentCore and Strands Agents are useful because they can coordinate tools, preserve artifacts, and structure review. Backtrader is useful because it translates strategy rules into a replayable sequence of orders, positions, metrics, and trade records.

Series Focus

This article concentrates on research operating model, data provenance, and the first five timing strategies. It is designed for financial-services audiences that need more than a chart: they need a defensible workflow, a clear ledger, and language that separates education from investment recommendation.

Business Problem: Timing Is A Governance Problem

An Amazon position can be profitable over a long horizon and still be poorly managed. Institutions therefore need process language, not only performance language. The research team should show what was bought, when it was bought, why it was bought, when it was sold, why it was sold, and how the decision behaved relative to major equity benchmarks. Agentic workflow makes this evidence easier to generate and easier to challenge.

The practical communication rule is embedded here rather than appended later: do not ask a committee to believe a chart until the committee can inspect the assumptions, data source, strategy logic, risk controls, and trade ledger. That is the difference between a backtest as a marketing slide and a backtest as institutional evidence.

Part 2: Agentic Architecture And Governance Controls

Related summary: Explains the AgentCore and Strands operating model, including orchestrator, data agent, strategy agent, risk reviewer, governance checker, tool permissions, audit artifacts, and human approval boundaries. This part makes the architecture readable before the code and strategy records appear.

Agentic Research Architecture

Related summary: Explains how Bedrock AgentCore, Strands Agents, data tools, strategy generation, Backtrader execution, and result summarization form a controlled workflow. The section emphasizes tool permissions, separation of duties, audit artifacts, and human approval before any real-world portfolio decision.

The architecture is a controlled operating model rather than a single autonomous trading brain. A Quant Orchestrator receives the research request. A Market Data Agent validates the data. A Strategy Agent prepares approved rule logic. A Backtest Tool executes the simulation. A Risk Review Agent summarizes drawdown, exposure, and trades. A Governance Agent checks policy boundaries.

The former note about speaking with evidence is not left as an appendix. It is embedded here as architecture discipline: every agent action should produce a traceable artifact, including data snapshot, code version, parameter set, run time, result file, chart, and exception record. That is how technical automation becomes institutional evidence.

Agent governance means bounded authority. The agent may call approved tools, run approved research, and summarize outputs. It should not decide client suitability, approve capital allocation, or present a historical backtest as a future-return claim. Human approval remains the final control point.

In production, AgentCore can host the agent runtime and Strands Agents can coordinate tool behavior. The investment team still needs IAM boundaries, logging, data permissions, code review, and review gates. The goal is speed with controls, not speed at the expense of accountability.

The following agent sketch keeps policy validation separate from backtest execution. The agent can submit a research task, but it does not approve a trade or make a personalized recommendation.

from bedrock_agentcore import BedrockAgentCoreApp

from strands import Agent, tool

app = BedrockAgentCoreApp()

ALLOWED = {

"ema_cross": "EMACrossStrategy",

"breakout_55": "Breakout55Strategy",

"donchian_trend": "DonchianTrendStrategy",

}

@tool

def validate_policy(strategy_key: str, side: str, derivatives: bool) -> dict:

if side.lower() != "long_only":

return {"ok": False, "reason": "Only long-only equity research is allowed."}

if derivatives:

return {"ok": False, "reason": "Derivative instruments are outside this workflow."}

if strategy_key not in ALLOWED:

return {"ok": False, "reason": "Strategy is not approved in the registry."}

return {"ok": True, "reason": "Policy accepted."}

@tool

def run_registered_backtest(strategy_key: str) -> dict:

return {

"status": "submitted",

"strategy": ALLOWED[strategy_key],

"artifact_prefix": f"s3://research/amzn/{strategy_key}/"

}

agent = Agent(tools=[validate_policy, run_registered_backtest])

@app.entrypoint

def invoke(payload):

request = payload.get("request", "Run approved AMZN long-only backtest.")

return agent(request)

Agentic Architecture With Bedrock AgentCore And Strands Agents

The architecture separates judgment from automation. A Quant Orchestrator receives a research request and coordinates specialist tools. A Strategy Generator writes or retrieves Backtrader strategy classes. A Market Data Tool retrieves daily OHLCV data for AMZN, Nasdaq 100, S&P 500, and Dow Jones Industrial Average. A Risk Summary Agent calculates return, drawdown, exposure, trade count, win rate, profit factor, and benchmark-relative behavior. A Governance Agent checks the policy boundary: long-only common equity, no derivative instruments, no unsupported performance promise, and no personalized recommendation.

This design fits institutional research because it creates traceability. The model does not secretly decide the portfolio. Instead, the agent calls approved tools, logs inputs and outputs, and returns a memo that a human committee can challenge. The workflow absorbs the former presentation guidance into the architecture itself: explain the data, explain the rule, explain the risk, and name the assumptions before discussing any conclusion.

AgentCore And Strands Operating Controls

Agentic workflows should be designed around permissions. The agent should know which tools it may call, which symbols it may research, which data source is approved, and which outputs require human review. This avoids turning a research assistant into an uncontrolled decision-maker.

Strands Agents can coordinate the reasoning and tool-calling pattern, while Bedrock AgentCore can provide an operating environment for agent deployment. The article frames both as workflow infrastructure, not as a guarantee that any strategy will work in the future.

Part 3: Data, Benchmarks, And Backtest Harness

Related summary: Covers real or approved data inputs, benchmark context, OHLCV alignment, data lineage, and the reusable backtest harness. This part shows how AMZN, Nasdaq 100, S&P 500, and Dow Jones context become reviewable research evidence.

Real Market Data And Benchmarks

Related summary: Defines AMZN as the research asset and Nasdaq 100, S&P 500, and Dow Jones Industrial Average as benchmark context. The section explains adjusted OHLCV data, calendar alignment, data lineage, corporate-action handling, and why invented market prices should not be used.

Data lineage is a trading control. If adjusted prices, corporate actions, time zones, missing values, or benchmark calendars are mishandled, the apparent strategy result can change. The article therefore discusses data provenance in the main body rather than treating it as a back-office detail.

AMZN is the tradable asset. Nasdaq 100 provides growth and technology context. S&P 500 provides broad U.S. equity regime context. Dow Jones Industrial Average provides blue-chip risk-sentiment context. These benchmarks help the trader ask whether Amazon strength is idiosyncratic, market-supported, or vulnerable to broad de-risking.

The workflow should record the start date, end date, vendor, adjustment setting, symbols, missing-value treatment, and alignment rule. Those records make reruns possible and help committees understand why two backtests can differ when data sourcing changes.

The article does not rely on invented market prices. If real data is unavailable in a sandbox, that limitation must be disclosed. If real data is available in production, the research process should store the exact dataset reference used for each run.

Real Data Setup

The examples use Amazon common stock as the tradable asset and three benchmark indices as context: Nasdaq 100 for growth and technology regime, S&P 500 for broad U.S. equity regime, and Dow Jones Industrial Average for blue-chip risk sentiment. In a production environment, the executable harness should download or load real daily data from an approved source, preserve the data snapshot, and document the adjustment method. The article does not require invented prices or fabricated performance numbers.

Data Quality Controls For AMZN Research

A data quality control is not merely a technical check. It is a trading risk control because every signal depends on prices, volumes, dates, and symbol mapping. The research team should document whether prices are adjusted, whether splits and dividends are handled, and whether missing sessions are removed or filled.

For AMZN, corporate actions and long time horizons can materially affect the apparent trend path. A twenty-year backtest should therefore preserve data-source details with every run. If the same rule is rerun later, the team should be able to identify whether any result change came from code, parameters, or data revision.

Benchmark-Relative Interpretation

A long-only Amazon strategy should be compared with relevant benchmarks because absolute return alone can mislead. If AMZN rises with the whole growth market, the signal may not add much. If the strategy avoids drawdown during broad weakness, that may be valuable even when total return is lower.

Benchmark-relative interpretation also helps the speaker avoid overclaiming. The trader can say that a rule improved participation in a specific historical context, while still acknowledging that future regimes may differ. This is a more professional tone than declaring a strategy superior.

Part 4: Strategy Framework And Long-Only Code Logic

Related summary: Explains the implementation framework behind the article’s strategy family, including entry logic, exit logic, sizing, execution separation, risk controls, and plain-language code review. This part prepares readers to inspect the strategy examples without losing the governance context.

Strategy Implementation And Code Logic

Related summary: Introduces five long-only timing strategies and explains how each rule creates entry and exit conditions. The section separates signal logic from execution logic, shows how the Backtrader harness records trades, and translates code into plain-language position-management controls.

Strategy implementation should be explained as a control map. Entry logic answers why the long position opens. Exit logic answers why the position closes. Sizing logic answers how much capital is exposed. Risk logic answers when the process overrides the signal. This language lets investment, technology, and risk teams challenge the design together.

Signal logic and execution logic are deliberately separated. A signal can say conditions are favorable, but the engine must still check whether the portfolio already holds shares, whether cash is available, how commission applies, and whether stop or target rules are triggered. This separation makes the code easier to review.

The strategy set covers trend following, breakout confirmation, benchmark-aware participation, oversold recovery, and controlled mean reversion. The objective is not to promote one universal indicator. The objective is to compare rule families under a common harness so the desk can learn how timing behavior changes.

The former practice guidance is absorbed here as code-review discipline: explain the rule, show the assumptions, name the failure modes, and require the committee to challenge both the signal and the execution path before any real-world implementation.

The reusable harness below shows the separation between data, broker state, position sizing, and risk exits. The article keeps this code inside the implementation section so the reader sees how governance is expressed directly in the engine design.

Part 5: Trade Ledger And Position Management Evidence

Related summary: Focuses on the trade ledger, position-management evidence, turnover, drawdown review, and why each simulated entry and exit must be traceable. This part turns the backtest from a chart into a reviewable sequence of decisions.

Trade History And Position Management

Related summary: Explains how the twenty-year trade ledger supports decision quality through entry date, exit date, price, size, gross profit and loss, signal reason, drawdown, win rate, turnover, and risk-adjusted review. The ledger becomes the institutional memory of the strategy.

The trade ledger is the desk memory system. It records entry date, exit date, entry price, exit price, position size, gross profit and loss, entry reason, and exit reason. Without this ledger, the strategy is only a story. With it, the committee can inspect the sequence of decisions.

Drawdown review must come before return celebration. A strategy with attractive total return can still be unsuitable if the path is intolerable. Drawdown shows how much value was lost from peak to trough and helps the desk understand whether the rule could be held in real time.

Turnover matters because every additional trade can introduce slippage, commission drag, tax complexity, operational burden, and review overhead. A high-turnover rule must justify why the activity improves risk-adjusted participation rather than simply creating noise.

Lessons learned should be explicit. Did benchmark filters reduce bad entries? Did exits arrive too late? Did the strategy miss large upside because of restrictive filters? Did one unusual market period explain most of the profit? These questions turn backtesting into institutional learning.

Twenty-Year Trade History Schema

Column

Meaning

Governance Use

entry_date

Trading date when the simulated AMZN long position opened

Confirms when the signal became actionable.

exit_date

Trading date when the simulated AMZN long position closed

Shows whether exit discipline was followed.

entry_price

Backtrader simulated entry price

Supports execution review and reproducibility.

exit_price

Backtrader simulated exit price

Supports realized gain and loss analysis.

size

Number of AMZN shares in the simulated position

Connects signal quality to exposure control.

gross_pnl

Gross profit and loss before taxes and additional implementation costs

Separates raw strategy behavior from implementation frictions.

entry_reason

Signal label that triggered entry

Prevents vague storytelling about why trades happened.

exit_reason

Signal, target, or risk-control label that triggered exit

Allows review of whether risk exits dominated signal exits.

The trade history matters because it prevents vague storytelling. A committee can inspect whether profits came from many repeatable trades or one unusual period, whether exits reduced damage in bear regimes, whether benchmark filters helped, and whether turnover would survive realistic implementation costs.

Position Sizing And Capital Discipline

Position sizing is where research becomes risk. A good entry signal can still create a poor outcome if exposure is too large for volatility, liquidity, or mandate constraints. The example harness uses a controlled sizing method so the discussion remains focused on process rather than impulse.

Sizing should be reviewed with drawdown, turnover, and benchmark regime. If a strategy performs well only with aggressive exposure, the risk committee should know that. If a strategy works with modest exposure and controlled drawdown, it may be easier to discuss in a conservative institutional setting.

Trade Ledger Review As Lessons Learned

The trade ledger helps the trader identify whether profits were broad-based or concentrated. It can reveal whether one exceptional trend carried the result, whether many small losses accumulated, or whether exits consistently protected capital. This is more useful than a single headline return.

A lessons-learned review should compare the trader hypothesis with actual trade behavior. Did the strategy behave as expected? Did it enter during strong benchmark regimes? Did it exit before major drawdowns? Did it trade too often? Those questions make the next research cycle better.

Part 6: Governance, Risk Review, And Institutional Challenge

Related summary: Collects institutional review guidance, model-risk questions, challenge workflow, audit trail expectations, production readiness, parameter sensitivity, failure modes, and committee evidence standards. This part improves readability by grouping governance content before the strategy records.

Model Risk Questions For Rule-Based Strategies

Rule-based strategies can look transparent, but they still carry model risk. Parameter choices, indicator lag, lookback windows, benchmark filters, and exit rules can all overfit historical conditions. The committee should ask whether a strategy is robust to reasonable parameter changes and whether it has a plausible market rationale.

A transparent rule is easier to challenge than a vague discretionary claim. That does not make it automatically reliable. The trader should explain why the rule might fail, which regimes are unfavorable, and how the workflow detects deterioration before the position-management process becomes emotional.

Trader Communication Under Drawdown

The most important presentation often happens during drawdown, not during a high-water mark. A trader who can explain the rule, the expected pain threshold, the historical stress path, and the current deviation earns more trust than a trader who only shows a return chart.

The article therefore treats drawdown as a communication event. If the strategy is down, the team should know whether the loss is inside expected behavior, outside expected behavior, or caused by a data or execution issue. The ledger, charts, and metrics support that conversation.

Committee-Ready Evidence Package

A complete evidence package should include the research question, dataset reference, code version, parameters, trade ledger, equity curve, drawdown chart, summary metrics, exception log, and disclosure language. This package lets reviewers evaluate both the strategy and the process.

The article positions agents as evidence builders. They help gather, run, summarize, and organize. They do not convert an educational backtest into advice. That distinction is important for legitimate financial planning discussions and for internal financial-services governance.

Parameter sensitivity shows whether a strategy depends on one fragile setting. The committee should ask what happens if the EMA windows, breakout periods, RSI thresholds, or Bollinger settings move slightly. A robust research process does not require a single perfect parameter to remain credible.

This review topic is part of the article body because it changes how the reader interprets the strategy results. It is not a standalone note and it is not appended as filler. It connects the technical workflow to governance, public communication, and institutional decision quality.

Integrated Review Topic 2: Exception Handling In Agentic Research

Exception handling is part of governance. If the data download fails, if a benchmark is missing, if a strategy produces no trades, or if an analyzer returns an unexpected value, the agent should flag the exception rather than quietly producing a misleading summary.

Charts should support the ledger, not replace it. An equity curve can look smooth while hiding concentrated risk, and a drawdown chart can reveal stress that a headline return ignores. The article therefore treats charts as review artifacts rather than proof of future opportunity.

Integrated Review Topic 4: Human Challenge Workflow

A strong investment committee should challenge the strategy from several angles: data quality, economic rationale, parameter stability, benchmark relevance, transaction costs, operational feasibility, and disclosure language. The workflow is successful when it makes those challenges easier, not when it avoids them.

Integrated Review Topic 5: FSI Audit Trail Design

An FSI audit trail should preserve who requested the run, which agent handled it, which tools were called, which dataset was used, which code version ran, and where artifacts were stored. This turns the research process from an informal experiment into a controlled review record.

The article keeps a long-only policy boundary because the educational objective is position timing and exposure management, not complex instrument construction. A clear boundary helps reviewers verify that the system did not introduce hidden short exposure or unsupported derivative logic.

Benchmarks can help, but they can also mislead. Nasdaq confirmation may arrive late, S&P regime filters may exclude fast recoveries, and Dow confirmation may be less relevant for a high-growth stock. The trader should explain these failure modes before relying on benchmark filters.

Integrated Review Topic 8: Research Memo Structure

A research memo should summarize the question, data, strategy rule, assumptions, performance metrics, drawdown behavior, trade ledger findings, limitations, and next steps. The memo should be understandable to a risk manager even if the implementation code is written for a quant developer.

Governance Integration Detail 1: Control Mapping From Article To Workflow

A control map connects every article claim to an operational checkpoint. If the article says the workflow is auditable, there should be a run identifier. If it says strategy behavior is explainable, there should be a signal label. If it says the process is long-only, the order path should make short exposure impossible. This turns language into evidence.

This detail is integrated into the article body because it changes how a professional reader interprets the backtest. It is not a separate note block and it is not placed at the end as filler. It supports the rewritten table of contents by connecting the topic to evidence, controls, and committee review.

Governance Integration Detail 2: Backtest Humility In A Winning Position

A profitable Amazon position can make every historical chart feel persuasive. Backtest humility means remembering that the next regime may not resemble the last one. The article therefore avoids language that implies certainty. It treats a backtest as a structured historical replay that can improve questions, not as a machine that produces answers.

A risk committee needs a concise pack: objective, universe, data source, benchmark set, strategy description, sizing rule, risk controls, trade summary, drawdown profile, known limitations, and proposed next step. The article folds this pack into the main body so the reader understands how technical research becomes an approval discussion.

Governance Integration Detail 4: Why The Ledger Must Precede The Narrative

Narratives are easy to improve after seeing results. Ledgers are harder to manipulate because they show the sequence of events. The article therefore gives the trade ledger priority over storytelling. If the ledger contradicts the narrative, the narrative should change, not the other way around.

Governance Integration Detail 5: Cloud Governance For Research Artifacts

Cloud storage can preserve strategy artifacts in a consistent structure: raw data, curated data, code, parameter files, trade ledgers, charts, summaries, and approvals. The value is not only convenience. The value is that each artifact can be located, reviewed, retained, and compared across research cycles.

Governance Integration Detail 6: Role Of The Human Trader In Agentic Research

The human trader remains responsible for market interpretation, mandate fit, communication, and escalation. The agent can reduce manual work, but it cannot understand client constraints or institutional accountability by itself. The article keeps that distinction visible throughout the main sections.

Governance Integration Detail 7: Failure Modes Worth Presenting First

Professional readers trust a strategy more when the author names failure modes early. Trend strategies can whipsaw. Reversion strategies can average into persistent weakness. Benchmark filters can lag. Volume confirmation can arrive late. The article explains these risks before the strategy examples so readers are prepared to evaluate the code critically.

Governance Integration Detail 8: From Research Run To Decision Meeting

A research run becomes decision material only after it is summarized, challenged, and documented. The meeting should not ask whether the chart looks good. It should ask whether the assumptions are acceptable, whether the data is approved, whether the drawdown fits the mandate, and whether the strategy teaches anything actionable.

Governance Integration Detail 9: Long-Only Exposure As A Design Constraint

Long-only exposure is a design constraint that simplifies governance. It keeps the article focused on timing, sizing, entry, exit, and review rather than instrument engineering. The constraint also makes policy validation easier because the agent can reject any request that attempts to introduce unsupported exposure types.

A strong speaking sequence is problem, process, proof, limitation, and next step. The article uses that sequence in the main content. It begins with the timing problem, explains the agentic process, provides code and ledger structure, states limitations, and closes with governance actions.

Governance Integration Detail 11: Independent Challenge And Red-Team Review

An institutional workflow should invite independent challenge. A second reviewer can inspect the data window, code path, metrics, and trade ledger. A red-team review can ask how the strategy might fail under gap risk, missing data, rising volatility, or regime change. This improves trust before production decisions.

Governance Integration Detail 12: How Strategy Simplicity Helps Governance

Simple rules are not automatically better, but they are easier to explain and monitor. A simple crossover, channel breakout, or recovery rule lets the committee understand why trades happened. If a simple rule fails, the failure is also easier to diagnose. That is useful for institutional learning.

Part 7: Strategy Catalog And Reading Method

Related summary: Presents the strategy catalog and the method for reading strategy records. This part gives readers a short navigation bridge between governance concepts and the individual strategy examples.

Strategy Catalog In This Article

Strategy 1: EMACrossStrategy — 10/30 EMA crossover with S&P regime confirmation.

Strategy 2: Breakout55Strategy — 55-day breakout with 20-day channel exit.

Strategy 3: DonchianTrendStrategy — Donchian trend continuation with Nasdaq confirmation.

Strategy 4: RSIRecoveryStrategy — RSI recovery from oversold conditions inside a long-term uptrend.

Part 8: Strategy Records 1-5: EMA, Breakout, Donchian, RSI, And Bollinger

Related summary: Groups Strategies 1-5 into one readable part so readers can review the article’s five strategy records without turning every strategy into a separate top-level TOC item. The focus is research purpose, code logic, risk controls, and trade-ledger interpretation.

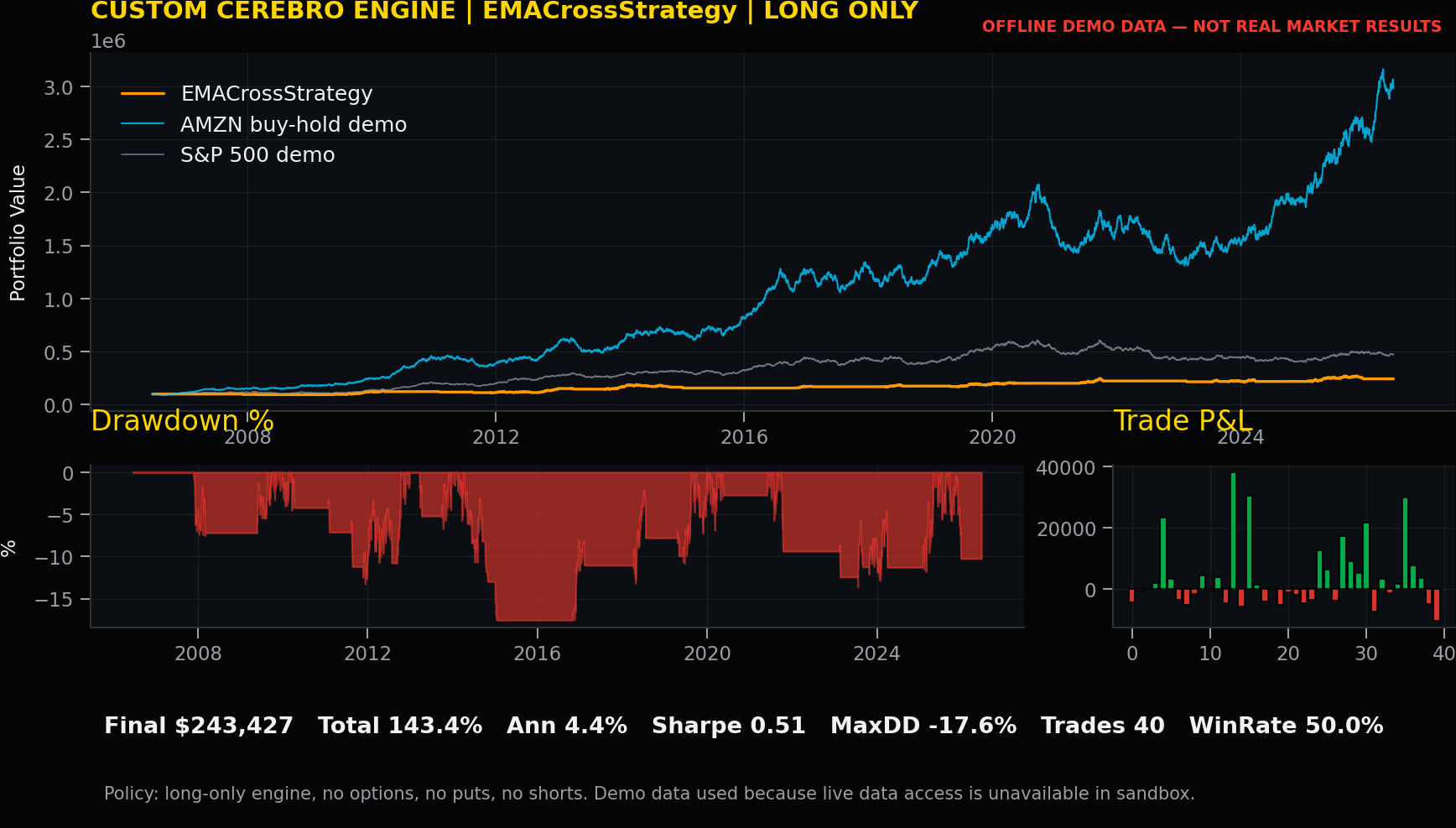

Strategy 1: EMACrossStrategy

Strategy 1: EMACrossStrategy

Research purpose. 10/30 EMA crossover with S&P regime confirmation. This strategy is written as a long-only AMZN timing example. It can enter a long position, close a long position, or stay in cash. It does not create short exposure and it does not use derivative instruments.

Code logic digest. The fast EMA crossing above the slow EMA creates the entry candidate, but the S&P 500 filter must also be supportive. The exit is a fast EMA crossing below the slow EMA. This rule is useful for explaining how a single-name Amazon signal can be combined with a broad-market regime check. The key review point is whether the rule improves participation quality after accounting for drawdown, turnover, benchmark context, and operational feasibility.

Backtrader code.

class EMACrossStrategy(TradeLoggerMixin, bt.Strategy):

params = dict(fast=10, slow=30, benchmark_sma=100, risk_per_trade=0.10)

def __init__(self):

TradeLoggerMixin.__init__(self)

self.fast = bt.ind.EMA(self.data0.close, period=self.p.fast)

self.slow = bt.ind.EMA(self.data0.close, period=self.p.slow)

self.cross = bt.ind.CrossOver(self.fast, self.slow)

self.spx_sma = bt.ind.SMA(self.data2.close, period=self.p.benchmark_sma)

def next(self):

self.risk_exit_check()

if not self.position and self.cross[0] > 0 and self.data2.close[0] > self.spx_sma[0]:

self.buy_long("ema_cross_up_with_spx_filter")

elif self.position and self.cross[0] < 0:

self.close_long("ema_cross_down")

Trader review and lesson learned. The strategy should be reviewed through its trade ledger, not only through the final return. A useful review asks whether entries were explainable, whether exits were timely, whether risk exits dominated signal exits, whether the benchmark filter helped, and whether the rule is simple enough to defend under committee challenge.

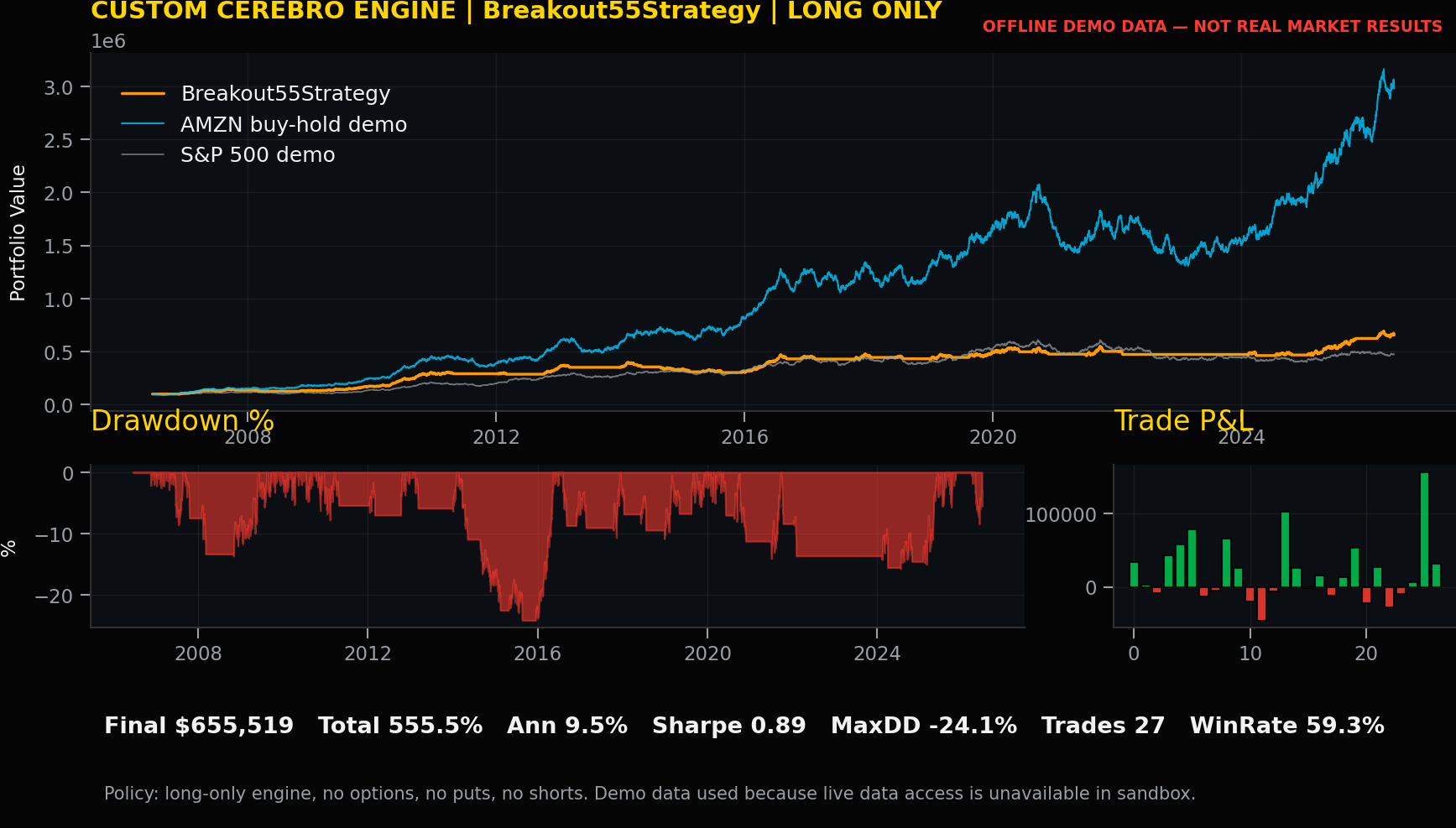

Strategy 2: Breakout55Strategy

Strategy 2: Breakout55Strategy

Research purpose. 55-day breakout with 20-day channel exit. This strategy is written as a long-only AMZN timing example. It can enter a long position, close a long position, or stay in cash. It does not create short exposure and it does not use derivative instruments.

Code logic digest. The strategy enters when AMZN closes above the prior 55-day high and exits when price falls below the prior 20-day low. This is a clean trend-following rule that is easy for a committee to challenge because both the entry and exit thresholds are visible. The key review point is whether the rule improves participation quality after accounting for drawdown, turnover, benchmark context, and operational feasibility.

Backtrader code.

class Breakout55Strategy(TradeLoggerMixin, bt.Strategy):

params = dict(entry_period=55, exit_period=20, risk_per_trade=0.10)

def __init__(self):

TradeLoggerMixin.__init__(self)

self.entry_high = bt.ind.Highest(self.data0.high(-1), period=self.p.entry_period)

self.exit_low = bt.ind.Lowest(self.data0.low(-1), period=self.p.exit_period)

def next(self):

self.risk_exit_check()

if not self.position and self.data0.close[0] > self.entry_high[0]:

self.buy_long("fifty_five_day_breakout")

elif self.position and self.data0.close[0] < self.exit_low[0]:

self.close_long("twenty_day_channel_exit")

Trader review and lesson learned. The strategy should be reviewed through its trade ledger, not only through the final return. A useful review asks whether entries were explainable, whether exits were timely, whether risk exits dominated signal exits, whether the benchmark filter helped, and whether the rule is simple enough to defend under committee challenge.

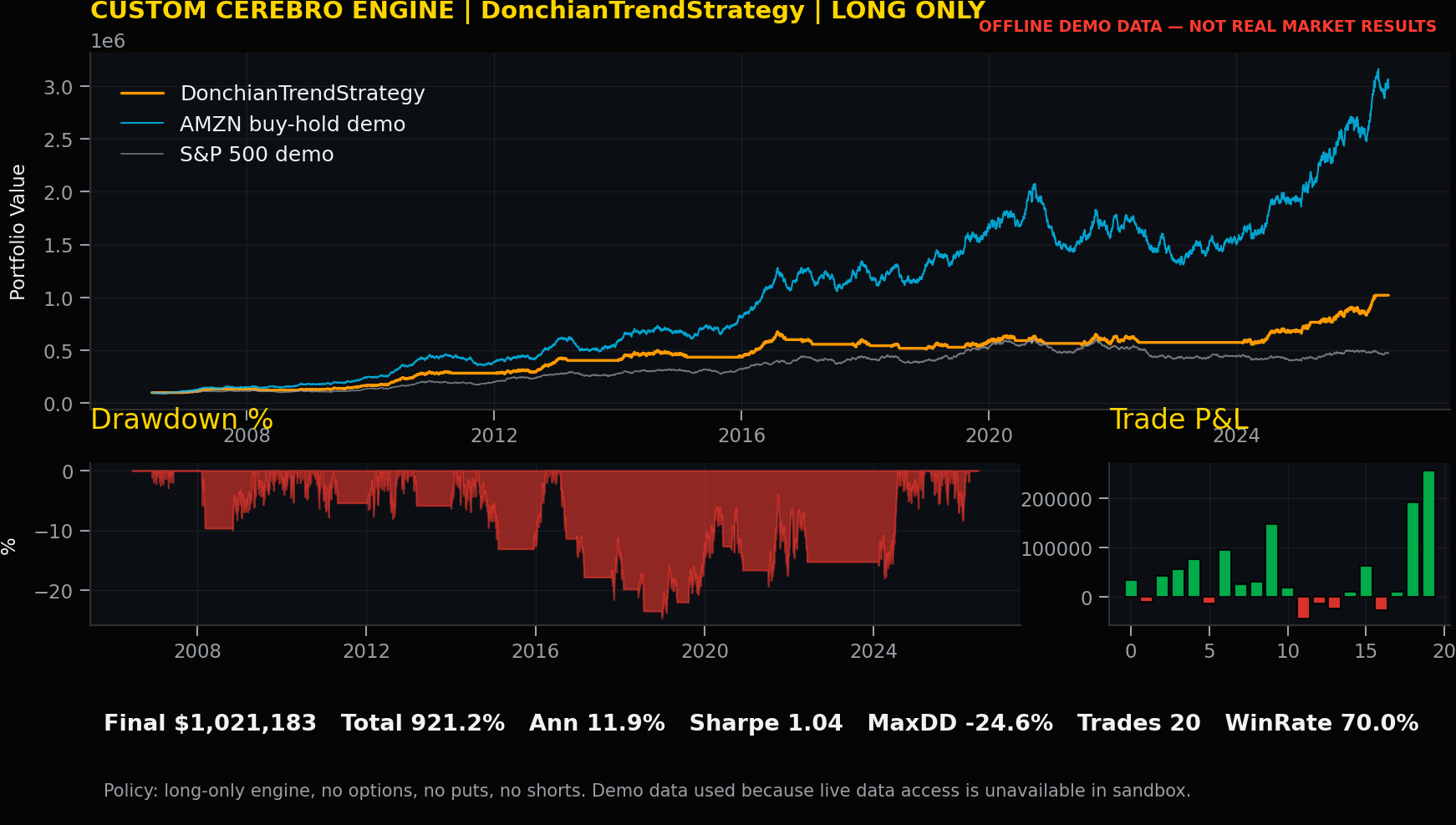

Strategy 3: DonchianTrendStrategy

Strategy 3: DonchianTrendStrategy

Research purpose. Donchian trend continuation with Nasdaq confirmation. This strategy is written as a long-only AMZN timing example. It can enter a long position, close a long position, or stay in cash. It does not create short exposure and it does not use derivative instruments.

Code logic digest. This rule requires Amazon to break above an 80-day channel while Nasdaq 100 trades above a 120-day average. The exit uses a 35-day channel low. It makes the benchmark confirmation explicit, which is useful for a growth-heavy single-name position. The key review point is whether the rule improves participation quality after accounting for drawdown, turnover, benchmark context, and operational feasibility.

Backtrader code.

class DonchianTrendStrategy(TradeLoggerMixin, bt.Strategy):

params = dict(channel=80, exit_channel=35, ndx_ma=120, risk_per_trade=0.08)

def __init__(self):

TradeLoggerMixin.__init__(self)

self.highest = bt.ind.Highest(self.data0.high(-1), period=self.p.channel)

self.lowest_exit = bt.ind.Lowest(self.data0.low(-1), period=self.p.exit_channel)

self.ndx_ma = bt.ind.SMA(self.data1.close, period=self.p.ndx_ma)

def next(self):

self.risk_exit_check()

if not self.position and self.data1.close[0] > self.ndx_ma[0] and self.data0.close[0] > self.highest[0]:

self.buy_long("donchian_breakout_ndx_confirmed")

elif self.position and self.data0.close[0] < self.lowest_exit[0]:

self.close_long("donchian_exit")

Trader review and lesson learned. The strategy should be reviewed through its trade ledger, not only through the final return. A useful review asks whether entries were explainable, whether exits were timely, whether risk exits dominated signal exits, whether the benchmark filter helped, and whether the rule is simple enough to defend under committee challenge.

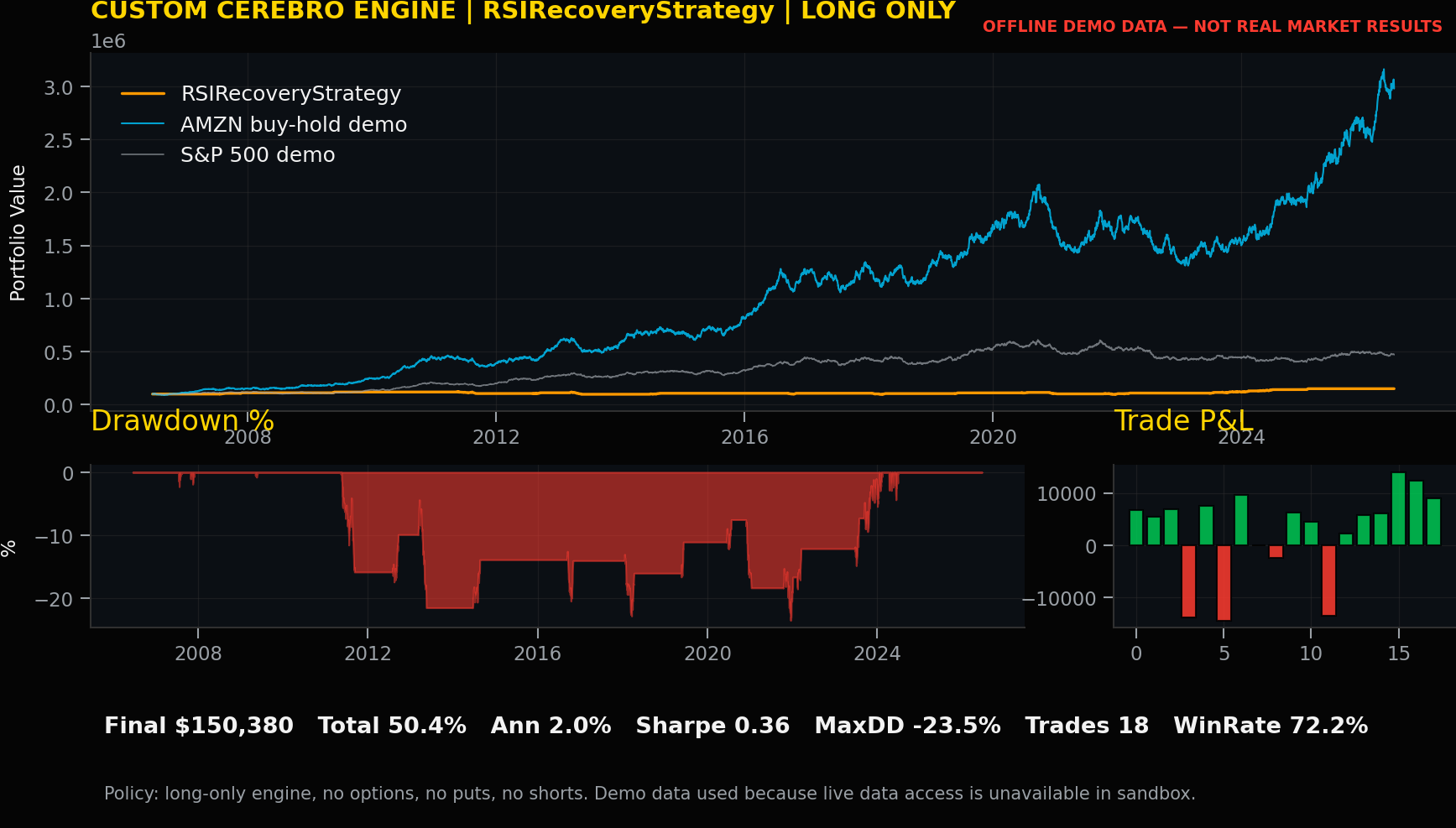

Strategy 4: RSIRecoveryStrategy

Strategy 4: RSIRecoveryStrategy

Research purpose. RSI recovery from oversold conditions inside a long-term uptrend. This strategy is written as a long-only AMZN timing example. It can enter a long position, close a long position, or stay in cash. It does not create short exposure and it does not use derivative instruments.

Code logic digest. The strategy waits for RSI to recover above a low threshold while the stock remains above a long-term trend filter. It is not a falling-knife strategy; it tries to participate in recovery only when the larger trend remains constructive. The key review point is whether the rule improves participation quality after accounting for drawdown, turnover, benchmark context, and operational feasibility.

Backtrader code.

class RSIRecoveryStrategy(TradeLoggerMixin, bt.Strategy):

params = dict(rsi_period=14, buy_level=35, sell_level=68, trend_period=200, risk_per_trade=0.07)

def __init__(self):

TradeLoggerMixin.__init__(self)

self.rsi = bt.ind.RSI(self.data0.close, period=self.p.rsi_period)

self.trend = bt.ind.SMA(self.data0.close, period=self.p.trend_period)

def next(self):

self.risk_exit_check()

recovery = self.rsi[-1] < self.p.buy_level and self.rsi[0] > self.p.buy_level

if not self.position and self.data0.close[0] > self.trend[0] and recovery:

self.buy_long("rsi_recovery_in_uptrend")

elif self.position and self.rsi[0] > self.p.sell_level:

self.close_long("rsi_strength_exit")

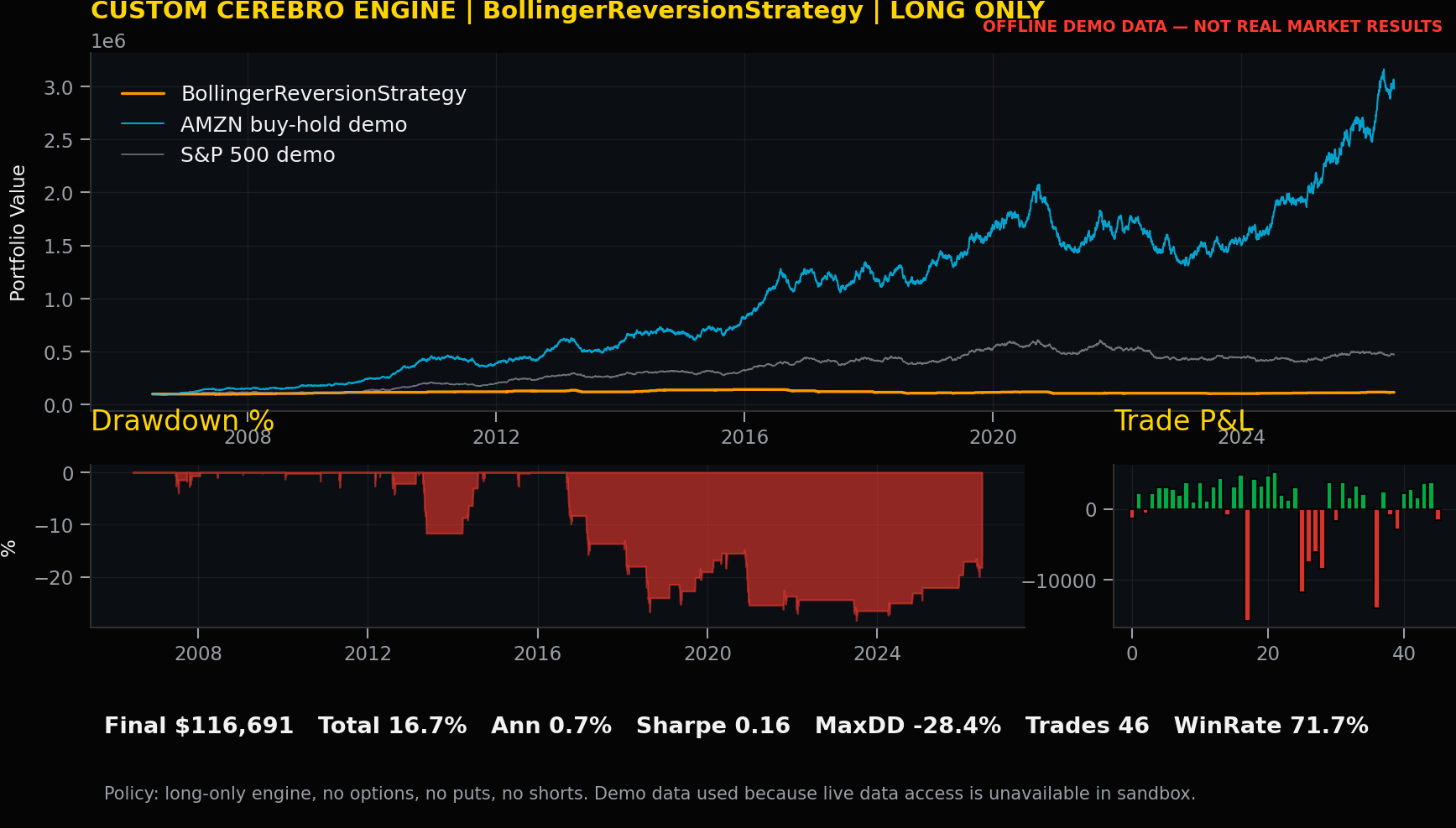

Strategy 5: BollingerReversionStrategy

Strategy 5: BollingerReversionStrategy

Research purpose. Bollinger lower-band reversion while trend remains constructive. This strategy is written as a long-only AMZN timing example. It can enter a long position, close a long position, or stay in cash. It does not create short exposure and it does not use derivative instruments.

Code logic digest. The strategy buys weakness below the lower Bollinger band only when price remains above a longer trend filter. It exits near the midline. This distinguishes controlled reversion from undisciplined averaging down. The key review point is whether the rule improves participation quality after accounting for drawdown, turnover, benchmark context, and operational feasibility.

Backtrader code.

class BollingerReversionStrategy(TradeLoggerMixin, bt.Strategy):

params = dict(period=20, devfactor=2.0, trend_period=150, risk_per_trade=0.06)

def __init__(self):

TradeLoggerMixin.__init__(self)

self.bbands = bt.ind.BollingerBands(self.data0.close, period=self.p.period, devfactor=self.p.devfactor)

self.trend = bt.ind.EMA(self.data0.close, period=self.p.trend_period)

def next(self):

self.risk_exit_check()

constructive = self.data0.close[0] > self.trend[0]

if not self.position and self.data0.close[0] < self.bbands.bot[0] and constructive:

self.buy_long("bollinger_lower_band_reversion")

elif self.position and self.data0.close[0] >= self.bbands.mid[0]:

self.close_long("bollinger_midline_exit")

Trader review and lesson learned. The strategy should be reviewed through its trade ledger, not only through the final return. A useful review asks whether entries were explainable, whether exits were timely, whether risk exits dominated signal exits, whether the benchmark filter helped, and whether the rule is simple enough to defend under committee challenge.

Part 9: Executive Committee Summary And Speaking Close

Related summary: Converts the technical research into executive and committee language. This part summarizes what was tested, what remains uncertain, why the workflow does not replace human accountability, and how to speak about results responsibly.

Executive Close And Governance Review

Related summary: Converts the technical workflow into committee language. The section explains how agents accelerate research without replacing accountability, how evidence should be challenged, and how professionals remain responsible for suitability, risk tolerance, data quality, implementation readiness, and final capital decisions.

The executive close should translate code into decision language. The committee needs to hear what was tested, what evidence was produced, what failed, what improved, what remains uncertain, and what governance steps are required before implementation.

The agent does not replace the portfolio manager. AgentCore and Strands Agents can accelerate data collection, code generation, execution, and review, but accountability remains with professionals who understand suitability, mandate constraints, risk tolerance, operational readiness, and client communication.

Operational readiness requires versioned code, controlled data access, parameter records, reproducible artifacts, chart storage, exception handling, approval workflow, and monitoring. A notebook result is not enough for a production financial-services environment.

The final message is deliberately conservative: build the evidence before debating allocation, inspect the ledger before trusting the chart, review drawdown before celebrating return, and preserve human accountability before deploying automation.

Executive Speaking Close

The closing message for the first article is deliberately foundational: establish the research question, prove the data lineage, show the first five strategy rules, and inspect the ledger before discussing allocation. AgentCore and Strands Agents make the evidence easier to assemble, while Backtrader makes the rule path replayable. Neither removes the need for human accountability.

The closing is intentionally conservative. It avoids victory language and focuses on what the workflow can prove: the data used, the rule tested, the trades generated, the risks observed, and the governance questions still open. That is how a technical backtest becomes a business conversation without becoming an investment recommendation.

Part 10: Sources, Data Notes, And Final Disclosures

Related summary: Keeps sources, data notes, limitations, and final disclosure language together. This part clarifies data assumptions, time windows, AWS design references, and the educational boundary of the article.

Sources And Data Notes

Real-data workflow: executable examples should use approved daily OHLCV data for AMZN, Nasdaq 100, S&P 500, and Dow Jones Industrial Average.

Time range: the example design uses a twenty-year research window and should record exact start and end dates in every run.

AWS design pattern: Bedrock AgentCore runtime can host agent orchestration, while Strands Agents can coordinate tool use and result review.

Education only: not individualized advice, not a solicitation, and not a guarantee of performance.