Build Benchmark-Relative Amazon Timing Systems Using Nasdaq, S&P 500, Dow, AgentCore, And Strands

Benchmark-relative AMZN research aligns signal quality with index beta, macro regime, liquidity risk, and portfolio exposure. Build long-only Backtrader examples using Nasdaq 100, S&P 500, and Dow Jones data, orchestrated by Amazon Bedrock AgentCore and Strands Agents for auditable, repeatable, FSI-grade investment research workflows and timing evidence across review committees.

Content presented here focuses exclusively on legitimate financial planning education, aiming to improve understanding of concepts, methodologies, and analytical approaches without promoting any specific securities, strategies, or market participation decisions.

No Personalized Advice:

No personalized recommendations, solicitations, or assurances are provided, and no guarantees of future performance, outcomes, or returns are implied, expressed, or otherwise suggested under any circumstances within this educational material.

Data Limitations:

Uploaded results rely on deterministic, offline data because live data was unavailable within the sandbox environment, and therefore outputs should be interpreted as illustrative examples rather than real time analyses.

Long-Only Scope:

All research language used is long only, avoiding options, puts, short selling, or bearish strategies, ensuring the discussion remains focused on traditional asset ownership and positive directional exposure concepts overall.

Opening: Measure AMZN Against Its Market Context

A long-only Amazon position should not be judged only by its own price path. AMZN competes for capital against growth benchmarks, broad U.S. equity exposure, and lower-volatility alternatives. This article therefore treats Nasdaq 100, S&P 500, and Dow Jones context as part of timing evidence, not as decoration around a stock chart.

Positioning

The voice here is a benchmark-aware portfolio operator. The article asks whether AMZN timing rules improve participation relative to relevant market regimes, whether benchmark filters reduce weak entries, and whether a committee can tell the difference between stock-specific evidence and broad beta.

The Client Problem Worth Solving

Benchmark-relative research prevents a profitable AMZN chart from becoming an unsupported skill claim. Investment teams need to know whether a rule added useful timing evidence versus Nasdaq 100 momentum, S&P 500 regime, and Dow risk sentiment. Risk teams need the same comparison to understand whether lower exposure, lower drawdown, or better relative strength drove the result.

Business Outcomes This Workflow Supports

The workflow helps committees discuss AMZN timing in relative rather than isolated terms. It supports benchmark-filter testing, calendar-aligned data review, relative-strength interpretation, and clearer explanations of whether a strategy reduced market risk, improved entry quality, or simply spent more time in cash.

Table Of Contents

Part 1: Opening Context And Article Focus Introduces the AMZN long-only timing problem, the article focus, and the business reason for creating evidence before debating any allocation decision. This part helps readers understand the trading voice, market context, and why the workflow is educational rather than advisory.

Part 2: Agentic Architecture And Governance Controls Explains the AgentCore and Strands operating model, including orchestrator, data agent, strategy agent, risk reviewer, governance checker, tool permissions, audit artifacts, and human approval boundaries. This part makes the architecture readable before the code and strategy records appear.

Part 3: Data, Benchmarks, And Backtest Harness Covers real or approved data inputs, benchmark context, OHLCV alignment, data lineage, and the reusable backtest harness. This part shows how AMZN, Nasdaq 100, S&P 500, and Dow Jones context become reviewable research evidence.

Part 4: Benchmark-Relative Strategy Framework And Code Logic Explains the implementation framework behind the article’s strategy family, including entry logic, exit logic, sizing, execution separation, risk controls, and plain-language code review. This part prepares readers to inspect the strategy examples without losing the governance context.

Part 5: Trade Ledger And Position Management Evidence Focuses on the trade ledger, position-management evidence, turnover, drawdown review, and why each simulated entry and exit must be traceable. This part turns the backtest from a chart into a reviewable sequence of decisions.

Part 6: Governance, Risk Review, And Institutional Challenge Collects institutional review guidance, model-risk questions, challenge workflow, audit trail expectations, production readiness, parameter sensitivity, failure modes, and committee evidence standards. This part improves readability by grouping governance content before the strategy records.

Part 7: Strategy Catalog And Reading Method Presents the strategy catalog and the method for reading strategy records. This part gives readers a short navigation bridge between governance concepts and the individual strategy examples.

Part 8: Strategy Records 11-15: Relative Strength, Regime, Dow, Keltner, And ADX Groups Strategies 11-15 into one readable part so readers can review the article’s five strategy records without turning every strategy into a separate top-level TOC item. The focus is research purpose, code logic, risk controls, and trade-ledger interpretation.

Part 9: Executive Committee Summary And Speaking Close Converts the technical research into executive and committee language. This part summarizes what was tested, what remains uncertain, why the workflow does not replace human accountability, and how to speak about results responsibly.

Part 10: Sources, Data Notes, And Final Disclosures Keeps sources, data notes, limitations, and final disclosure language together. This part clarifies data assumptions, time windows, AWS design references, and the educational boundary of the article.

Part 1: Opening Context And Article Focus

Related summary: Introduces the AMZN long-only timing problem, the article focus, and the business reason for creating evidence before debating any allocation decision. This part helps readers understand the trading voice, market context, and why the workflow is educational rather than advisory.

Opening And Market Context

Related summary: Establishes the AMZN timing problem, explains why backtesting belongs in institutional review, and frames the article as evidence generation rather than prediction. The section connects a profitable long-only position to risk discipline, benchmark awareness, disclosure language, and committee-ready communication.

A strong article begins with the trading problem, not the software. A long-only Amazon position can be profitable and still suffer from weak timing, unclear exit discipline, and oversized exposure. This section therefore frames backtesting as a governance tool that helps the desk explain decisions before debating allocation.

The useful content from the former delivery note is digested here: speak with evidence, name assumptions, and avoid certainty. The audience should hear what the workflow tests, what data supports it, what could fail, and what remains a human decision. That is stronger than attaching a repeated practice paragraph at the end.

Market context matters because AMZN is affected by growth appetite, broad equity regime, consumer expectations, cloud sentiment, liquidity, and valuation pressure. Benchmark awareness helps the trader avoid claiming that every gain comes from stock-specific skill.

Series Focus

This article concentrates on benchmark-relative signals, market filters, and risk-controlled participation. It is one part of a four-post technical series. The structure is publication-ready and avoids exposing draft instructions. It keeps the speaking-coach intent while turning the message into polished sections for financial-services audiences.

Business Problem: Timing Is A Governance Problem

An Amazon position can be profitable over a long horizon and still be poorly managed. Institutions therefore need process language, not only performance language. The research team should show what was bought, when it was bought, why it was bought, when it was sold, why it was sold, and how the decision behaved relative to major equity benchmarks. The agentic workflow makes this evidence easier to generate and easier to challenge.

Part 2: Agentic Architecture And Governance Controls

Related summary: Explains the AgentCore and Strands operating model, including orchestrator, data agent, strategy agent, risk reviewer, governance checker, tool permissions, audit artifacts, and human approval boundaries. This part makes the architecture readable before the code and strategy records appear.

Agentic Research Architecture

Related summary: Explains how Bedrock AgentCore, Strands Agents, data tools, strategy generation, Backtrader execution, and result summarization form a controlled workflow. The section emphasizes tool permissions, separation of duties, audit artifacts, and human approval before any real-world portfolio decision.

The agentic architecture separates responsibilities. The orchestrator receives the request, the data tool validates OHLCV inputs, the strategy generator prepares rule logic, the Backtrader tool executes the simulation, the risk reviewer summarizes drawdown and trade behavior, and the governance checker validates policy boundaries.

The digested delivery rule appears as architecture discipline: every agent action should produce evidence. A useful run leaves a data reference, code version, parameters, timestamps, trade ledger, metrics, chart path, and exception record. These artifacts make the output reviewable by investment, technology, and risk teams.

AgentCore and Strands Agents can accelerate the research loop, but bounded authority is essential. The system can run approved tools and prepare a memo; it should not decide suitability, approve capital allocation, or convert a historical backtest into a performance promise.

Agentic Architecture With Bedrock AgentCore And Strands Agents

The architecture separates judgment from automation. A Quant Orchestrator receives a research request and coordinates specialist tools. A Strategy Generator writes or retrieves Backtrader strategy classes. A Market Data Tool retrieves daily OHLCV data for AMZN, ^NDX, ^GSPC, and ^DJI. A Risk Summary Agent calculates return, drawdown, exposure, trade count, win rate, profit factor, and benchmark-relative behavior. A Governance Agent checks the policy boundary: long-only common equity, no derivatives, no unsupported performance promise.

This design fits institutional research because it creates traceability. The model does not secretly decide the portfolio. Instead, the agent calls approved tools, logs inputs and outputs, and returns a memo that a human committee can challenge. The code examples use Backtrader because it provides an event-driven research engine, technical indicators, analyzers, order handling, and trade statistics.

Agent Runtime Sketch

Part 3: Data, Benchmarks, And Backtest Harness

Related summary: Covers real or approved data inputs, benchmark context, OHLCV alignment, data lineage, and the reusable backtest harness. This part shows how AMZN, Nasdaq 100, S&P 500, and Dow Jones context become reviewable research evidence.

Real Market Data And Benchmarks

Related summary: Defines AMZN as the research asset and Nasdaq 100, S&P 500, and Dow Jones Industrial Average as benchmark context. The section explains adjusted OHLCV data, calendar alignment, data lineage, corporate-action handling, and why invented market prices should not be used.

Data lineage is a trading control. Adjusted prices, corporate actions, missing values, holiday calendars, vendor changes, and benchmark alignment can all change the apparent behavior of a timing rule. This section treats data engineering as part of investment governance rather than as a background task.

AMZN is the tradable asset. Nasdaq 100, S&P 500, and Dow Jones Industrial Average provide different lenses for growth regime, broad equity risk, and blue-chip sentiment. The workflow should document why each benchmark is used and where each benchmark might mislead.

The article avoids invented prices and unsupported performance claims. If data cannot be retrieved, the limitation should be stated. If production data is used, the dataset snapshot and adjustment policy should be preserved with the backtest artifacts.

Real Data Setup

The examples use Amazon common stock as the tradable asset and three benchmark indices as context: Nasdaq 100 for growth and technology regime, S&P 500 for broad U.S. equity regime, and Dow Jones Industrial Average for blue-chip risk sentiment. The executable harness downloads real daily data through yfinance when run in your environment. The article does not invent market prices or fabricated performance numbers.

Reusable Backtrader Harness For Twenty-Year Trade History

Part 4: Benchmark-Relative Strategy Framework And Code Logic

Related summary: Explains the implementation framework behind the article’s strategy family, including entry logic, exit logic, sizing, execution separation, risk controls, and plain-language code review. This part prepares readers to inspect the strategy examples without losing the governance context.

Benchmark-Relative Strategy Implementation And Code Logic

Related summary: Introduces the strategy examples used in this article and explains how each rule creates entry and exit conditions. The section separates signal logic from execution logic and translates code into plain-language position-management controls.

Strategy implementation should read like a control map. Entry logic explains why a long position opens. Exit logic explains why it closes. Sizing logic explains how much exposure is taken. Risk logic explains when the process overrides the signal. This makes code review accessible to non-developers.

Signal logic and execution logic should remain separate. A signal can identify favorable conditions, but the execution engine must check existing position state, available cash, commission, risk stops, and target exits. Separation improves auditability and reduces hidden behavior.

The article includes code talk inside the main strategy discussion rather than as detached notes. Each strategy should be judged by its ledger, drawdown, turnover, benchmark behavior, and operational feasibility, not by a headline return alone.

This article specifically focuses on benchmark-relative signals, Nasdaq confirmation, S&P regime filters, Dow risk checks, and relative-strength interpretation. The code review should therefore evaluate whether the strategy family supports that business objective and whether its trade records are explainable enough for institutional review.

Part 5: Trade Ledger And Position Management Evidence

Related summary: Focuses on the trade ledger, position-management evidence, turnover, drawdown review, and why each simulated entry and exit must be traceable. This part turns the backtest from a chart into a reviewable sequence of decisions.

Relative-Strength Records And Position Management

Related summary: Explains how the trade ledger supports position-management decisions by recording entries, exits, prices, sizes, realized profit and loss, signal reasons, drawdown behavior, turnover, and risk-adjusted review.

The trade ledger is the desk memory system. It records entry date, exit date, price, size, gross profit and loss, entry reason, and exit reason. Without a ledger, the strategy is only a story. With a ledger, the committee can inspect the actual sequence of simulated decisions.

Drawdown review must come before return celebration. A strategy can look attractive in total return while being difficult to hold through real stress. The ledger and drawdown path help reviewers decide whether the rule fits the mandate and risk tolerance.

The former practice-note message is digested into the review process: explain the data source, date range, strategy rule, benchmark context, risk metric, and ledger before any conclusion. The article keeps this inside the position-management section because it changes how the evidence should be read.

Twenty-Year Trade History Schema

Column

Meaning

entry_date

Trading date when the simulated AMZN long position opened

exit_date

Trading date when the simulated AMZN long position closed

entry_price

Backtrader simulated entry price

exit_price

Backtrader simulated exit price

size

Number of AMZN shares in the simulated position

gross_pnl

Gross profit and loss before taxes and additional implementation costs

entry_reason

Signal label that triggered entry

exit_reason

Signal, target, or risk-control label that triggered exit

The trade history matters because it prevents vague storytelling. A committee can inspect whether profits came from many repeatable trades or one unusual period, whether exits reduced damage in bear regimes, whether benchmark filters helped, and whether turnover would survive realistic implementation costs.

Part 6: Governance, Risk Review, And Institutional Challenge

Related summary: Collects institutional review guidance, model-risk questions, challenge workflow, audit trail expectations, production readiness, parameter sensitivity, failure modes, and committee evidence standards. This part improves readability by grouping governance content before the strategy records.

Illustrative pattern; adapt IAM, networking, approvals, and logging for production.

from bedrock_agentcore import BedrockAgentCoreApp

from strands import Agent, tool

app = BedrockAgentCoreApp()

ALLOWED = {

"breakout_55": "Breakout55Strategy",

"ema_cross": "EMACrossStrategy",

"multi_factor": "MultiFactorEnsembleStrategy",

}

@tool

def validate_policy(strategy_key: str, side: str, derivatives: bool) -> dict:

if side.lower() != "long_only":

return {"ok": False, "reason": "Only long-only equity research is allowed."}

if derivatives:

return {"ok": False, "reason": "Derivative instruments are outside this workflow."}

if strategy_key not in ALLOWED:

return {"ok": False, "reason": "Strategy is not approved in the registry."}

return {"ok": True, "reason": "Policy accepted."}

@tool

def run_registered_backtest(strategy_key: str) -> dict:

return {"status": "submitted", "strategy": ALLOWED[strategy_key], "artifact_prefix": f"s3://research/amzn/{strategy_key}/"}

agent = Agent(tools=[validate_policy, run_registered_backtest])

@app.entrypoint

def invoke(payload):

return agent(payload.get("request", "Run approved AMZN long-only backtest."))

if __name__ == "__main__":

app.run()

Benchmark-relative research begins with benchmark selection. Nasdaq 100, S&P 500, and Dow Jones Industrial Average answer different questions. The article explains why each index is used, what it confirms, and where it can mislead the reader.

Applied Main-Article Detail 2: Relative Strength Versus Absolute Return

A stock can rise and still underperform its opportunity set. Relative strength asks whether AMZN earns its place against technology and broad-equity alternatives. This changes the conversation from simple profit to disciplined capital allocation.

The S&P 500 regime filter is a broad-risk lens. It can help avoid weak market environments, but it can also exclude fast recoveries. The article describes this tradeoff so benchmark filters are treated as assumptions, not as unquestioned truth.

Dow confirmation is not a perfect match for a high-growth single name, yet it can show broader risk appetite. The trader should explain that this input is a context variable and should be tested against other market-regime definitions.

Relative comparison requires calendar alignment. If AMZN and benchmark series are not aligned, signals can be shifted or distorted. The article brings this data-engineering point into the main content because benchmark research depends on clean time alignment.

Applied Main-Article Detail 6: Committee Interpretation Of Relative Results

A committee should ask whether benchmark-relative logic reduced drawdown, improved entry timing, or simply reduced exposure. Lower return with lower drawdown may be acceptable in one mandate and unacceptable in another. The article keeps that mandate question visible.

A complete evidence package should include the research question, data source, adjustment policy, symbol list, code version, parameter set, trade ledger, drawdown profile, metrics summary, exception log, and disclosure language. This makes the backtest reviewable across investment, risk, technology, and compliance teams.

Institutional Review Lens 2: Human Challenge Workflow

The workflow is successful when it invites challenge. Reviewers should ask whether the data is clean, the rule has economic rationale, the benchmark is appropriate, the parameters are stable, the costs are realistic, and the conclusion is limited to what the evidence supports.

The article keeps the policy boundary long-only. That boundary focuses the workflow on timing, sizing, exits, and evidence quality rather than complex instrument construction. It also gives the governance agent a clear rule for rejecting unsupported requests.

Institutional Review Lens 4: Chart And Ledger Interpretation

Charts are useful, but the ledger is the audit trail. An equity curve can hide concentration, and a single return number can hide turnover. The article therefore treats charts, ledgers, and metrics as complementary evidence, not as interchangeable proof.

Institutional Review Lens 5: Production Readiness Checklist

A notebook is not production. Production readiness requires controlled data access, versioned code, parameter records, repeatable runs, exception handling, artifact storage, approval workflow, and monitoring. Agentic tooling should support those controls rather than bypass them.

Professional articles should name failure modes early. Trend rules can whipsaw, momentum can exhaust, volatility filters can lag, and benchmark filters can exclude fast recoveries. Naming these risks increases credibility and helps the committee prepare useful questions.

Part 7: Strategy Catalog And Reading Method

Related summary: Presents the strategy catalog and the method for reading strategy records. This part gives readers a short navigation bridge between governance concepts and the individual strategy examples.

Strategy Review Method Before Reading The Records

Before reading the strategy records, use the same evidence sequence for every rule: confirm the data, identify the entry condition, identify the exit condition, inspect the sizing assumption, review drawdown, compare benchmark behavior, and record the lesson learned. This sentence replaces the repeated delivery note by turning it into a method used inside the article.

Strategy Catalog In This Article

Strategy 11: RelativeStrengthNDXStrategy — AMZN relative strength versus Nasdaq 100.

Part 8: Strategy Records 11-15: Relative Strength, Regime, Dow, Keltner, And ADX

Related summary: Groups Strategies 11-15 into one readable part so readers can review the article’s five strategy records without turning every strategy into a separate top-level TOC item. The focus is research purpose, code logic, risk controls, and trade-ledger interpretation.

Strategy 11: RelativeStrengthNDXStrategy

Strategy 11: RelativeStrengthNDXStrategy

Research purpose. AMZN relative strength versus Nasdaq 100. This strategy is written as a long-only AMZN timing example. It can enter a long position, close a long position, or stay in cash. It does not create short exposure and it does not use options, puts, swaps, futures, margin, or other derivative instruments.

Position-management review. For RelativeStrengthNDXStrategy, the desk should evaluate whether amzn relative strength versus nasdaq 100 adds useful timing evidence after costs, drawdown, and benchmark context. The review should inspect how often the rule trades, whether exits are understandable, whether the holding period fits the mandate, and whether the signal contributes insight beyond simply holding AMZN through every regime.

Backtrader code. Add this class below the reusable harness, then run run_backtest(RelativeStrengthNDXStrategy, "RelativeStrengthNDXStrategy") in a controlled research environment.

class RelativeStrengthNDXStrategy(TradeLoggerMixin, bt.Strategy):

params = dict(rs_period=90, risk_per_trade=0.08)

def __init__(self):

TradeLoggerMixin.__init__(self)

self.rs = self.data0.close / self.data1.close

self.rs_ma = bt.ind.SMA(self.rs, period=self.p.rs_period)

def next(self):

self.risk_exit_check()

if not self.position and self.rs[0] > self.rs_ma[0] and self.rs[-1] <= self.rs_ma[-1]:

self.buy_long("amzn_relative_strength_vs_ndx")

elif self.position and self.rs[0] < self.rs_ma[0]:

self.close_long("relative_strength_fade")

The agent review for RelativeStrengthNDXStrategy should summarize the signal path, ledger completeness, risk-control activity, and long-only policy status for this specific strategy run.

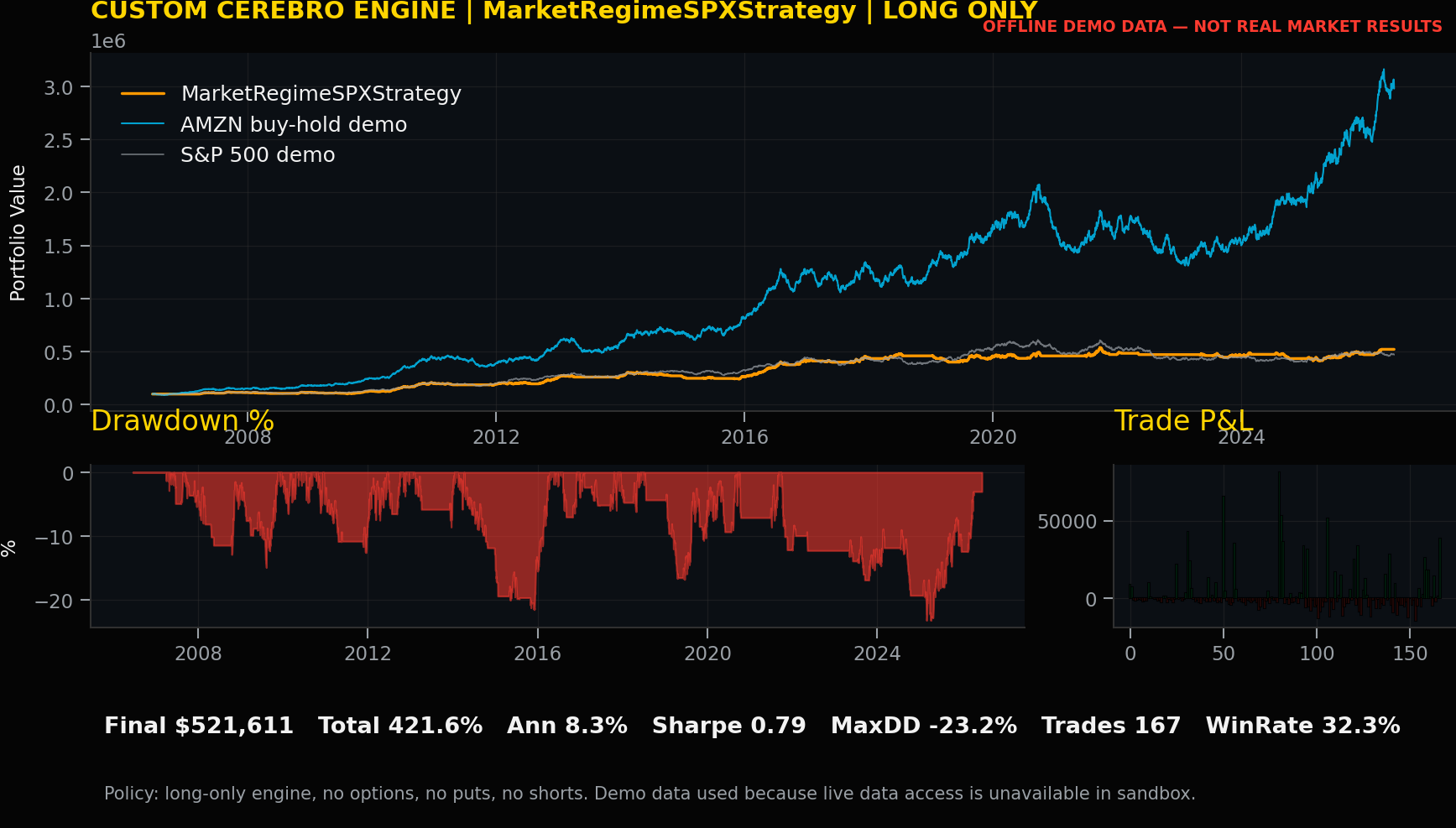

Strategy 12: MarketRegimeSPXStrategy

Strategy 12: MarketRegimeSPXStrategy

Research purpose. S&P 500 regime filter with AMZN momentum. This strategy is written as a long-only AMZN timing example. It can enter a long position, close a long position, or stay in cash. It does not create short exposure and it does not use options, puts, swaps, futures, margin, or other derivative instruments.

Position-management review. For MarketRegimeSPXStrategy, the desk should evaluate whether s&p 500 regime filter with amzn momentum adds useful timing evidence after costs, drawdown, and benchmark context. The review should inspect how often the rule trades, whether exits are understandable, whether the holding period fits the mandate, and whether the signal contributes insight beyond simply holding AMZN through every regime.

Backtrader code. Add this class below the reusable harness, then run run_backtest(MarketRegimeSPXStrategy, "MarketRegimeSPXStrategy") in a controlled research environment.

class MarketRegimeSPXStrategy(TradeLoggerMixin, bt.Strategy):

params = dict(spx_period=200, amzn_period=50, risk_per_trade=0.08)

def __init__(self):

TradeLoggerMixin.__init__(self)

self.spx_ma = bt.ind.SMA(self.data2.close, period=self.p.spx_period)

self.amzn_ma = bt.ind.SMA(self.data0.close, period=self.p.amzn_period)

def next(self):

self.risk_exit_check()

regime_ok = self.data2.close[0] > self.spx_ma[0]

if not self.position and regime_ok and self.data0.close[0] > self.amzn_ma[0]:

self.buy_long("spx_regime_amzn_momentum")

elif self.position and (not regime_ok or self.data0.close[0] < self.amzn_ma[0]):

self.close_long("regime_or_momentum_exit")

The agent review for MarketRegimeSPXStrategy should summarize the signal path, ledger completeness, risk-control activity, and long-only policy status for this specific strategy run.

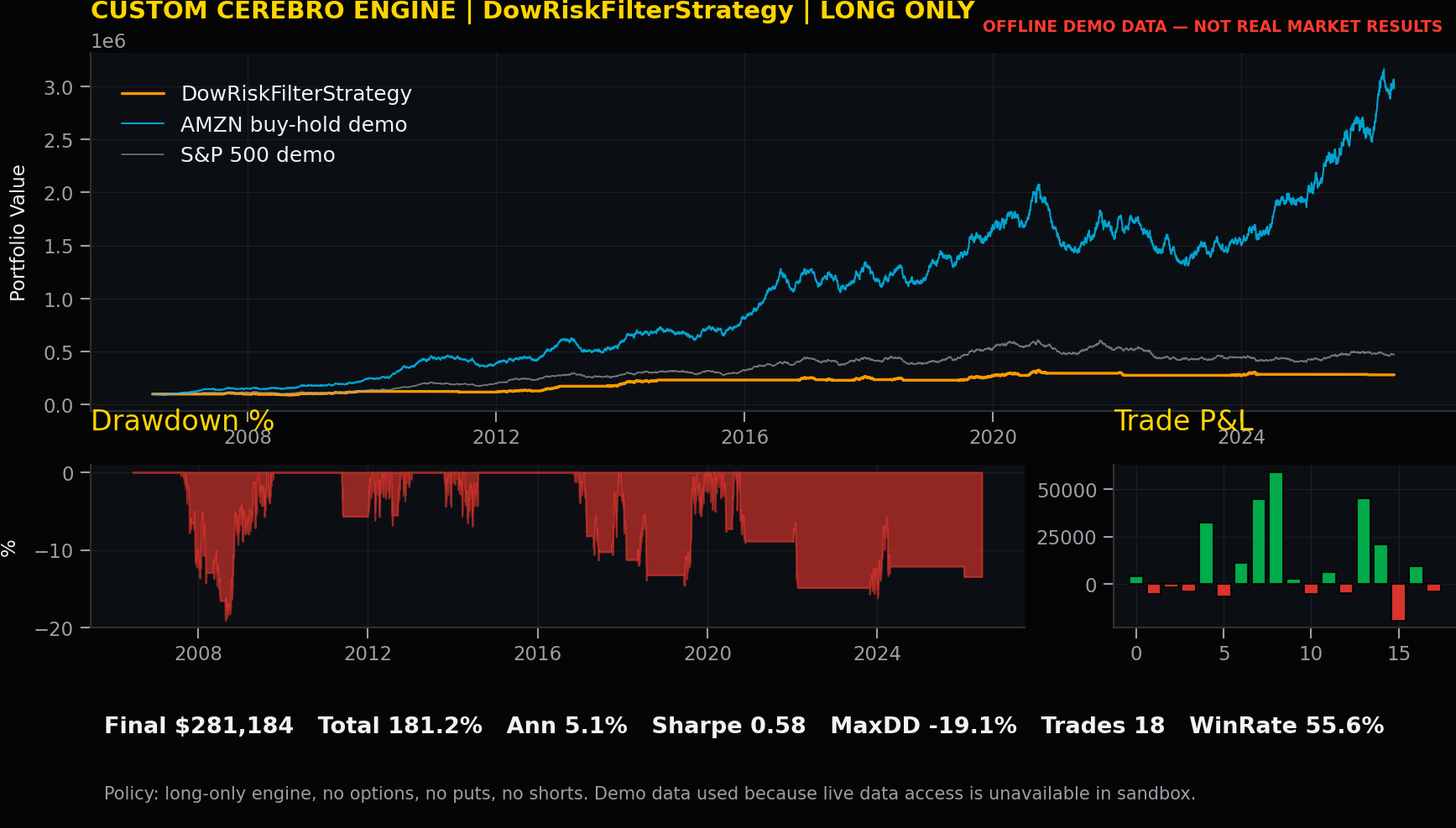

Strategy 13: DowRiskFilterStrategy

Strategy 13: DowRiskFilterStrategy

Research purpose. Dow Jones trend filter with AMZN entry signal. This strategy is written as a long-only AMZN timing example. It can enter a long position, close a long position, or stay in cash. It does not create short exposure and it does not use options, puts, swaps, futures, margin, or other derivative instruments.

Position-management review. For DowRiskFilterStrategy, the desk should evaluate whether dow jones trend filter with amzn entry signal adds useful timing evidence after costs, drawdown, and benchmark context. The review should inspect how often the rule trades, whether exits are understandable, whether the holding period fits the mandate, and whether the signal contributes insight beyond simply holding AMZN through every regime.

Backtrader code. Add this class below the reusable harness, then run run_backtest(DowRiskFilterStrategy, "DowRiskFilterStrategy") in a controlled research environment.

class DowRiskFilterStrategy(TradeLoggerMixin, bt.Strategy):

params = dict(dow_period=150, amzn_fast=20, amzn_slow=80, risk_per_trade=0.07)

def __init__(self):

TradeLoggerMixin.__init__(self)

self.dow_ma = bt.ind.EMA(self.data3.close, period=self.p.dow_period)

self.fast = bt.ind.EMA(self.data0.close, period=self.p.amzn_fast)

self.slow = bt.ind.EMA(self.data0.close, period=self.p.amzn_slow)

self.cross = bt.ind.CrossOver(self.fast, self.slow)

def next(self):

self.risk_exit_check()

if not self.position and self.data3.close[0] > self.dow_ma[0] and self.cross[0] > 0:

self.buy_long("dow_risk_filter_amzn_cross")

elif self.position and self.cross[0] < 0:

self.close_long("amzn_cross_exit")

The agent review for DowRiskFilterStrategy should summarize the signal path, ledger completeness, risk-control activity, and long-only policy status for this specific strategy run.

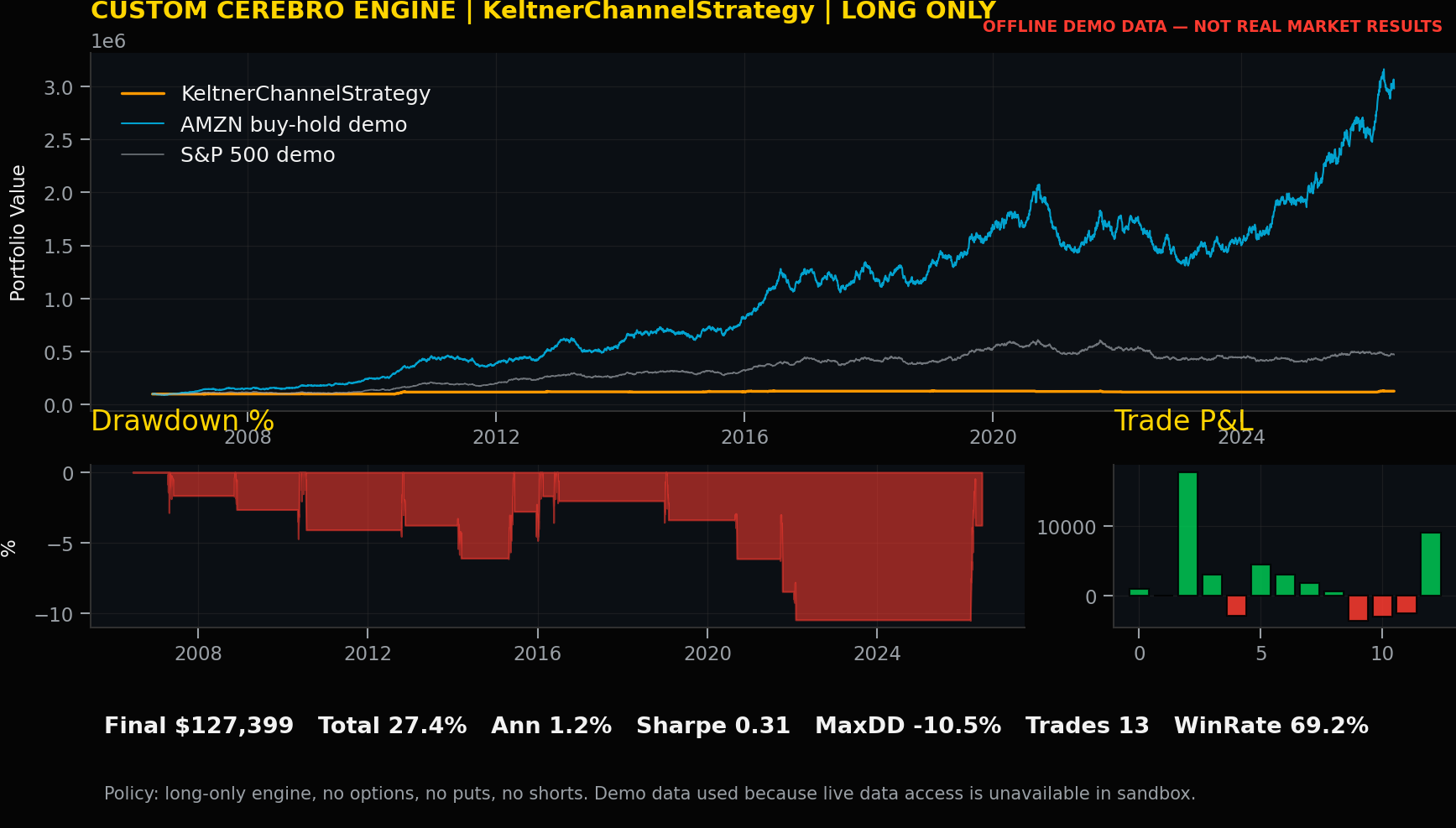

Strategy 14: KeltnerChannelStrategy

Strategy 14: KeltnerChannelStrategy

Research purpose. Keltner channel trend entry. This strategy is written as a long-only AMZN timing example. It can enter a long position, close a long position, or stay in cash. It does not create short exposure and it does not use options, puts, swaps, futures, margin, or other derivative instruments.

Position-management review. For KeltnerChannelStrategy, the desk should evaluate whether keltner channel trend entry adds useful timing evidence after costs, drawdown, and benchmark context. The review should inspect how often the rule trades, whether exits are understandable, whether the holding period fits the mandate, and whether the signal contributes insight beyond simply holding AMZN through every regime.

Backtrader code. Add this class below the reusable harness, then run run_backtest(KeltnerChannelStrategy, "KeltnerChannelStrategy") in a controlled research environment.

class KeltnerChannelStrategy(TradeLoggerMixin, bt.Strategy):

params = dict(ema_period=20, atr_period=10, mult=1.8, risk_per_trade=0.08)

def __init__(self):

TradeLoggerMixin.__init__(self)

self.ema = bt.ind.EMA(self.data0.close, period=self.p.ema_period)

self.atr = bt.ind.ATR(self.data0, period=self.p.atr_period)

self.upper = self.ema + self.p.mult * self.atr

def next(self):

self.risk_exit_check()

if not self.position and self.data0.close[0] > self.upper[0]:

self.buy_long("keltner_upper_break")

elif self.position and self.data0.close[0] < self.ema[0]:

self.close_long("keltner_ema_exit")

The agent review for KeltnerChannelStrategy should summarize the signal path, ledger completeness, risk-control activity, and long-only policy status for this specific strategy run.

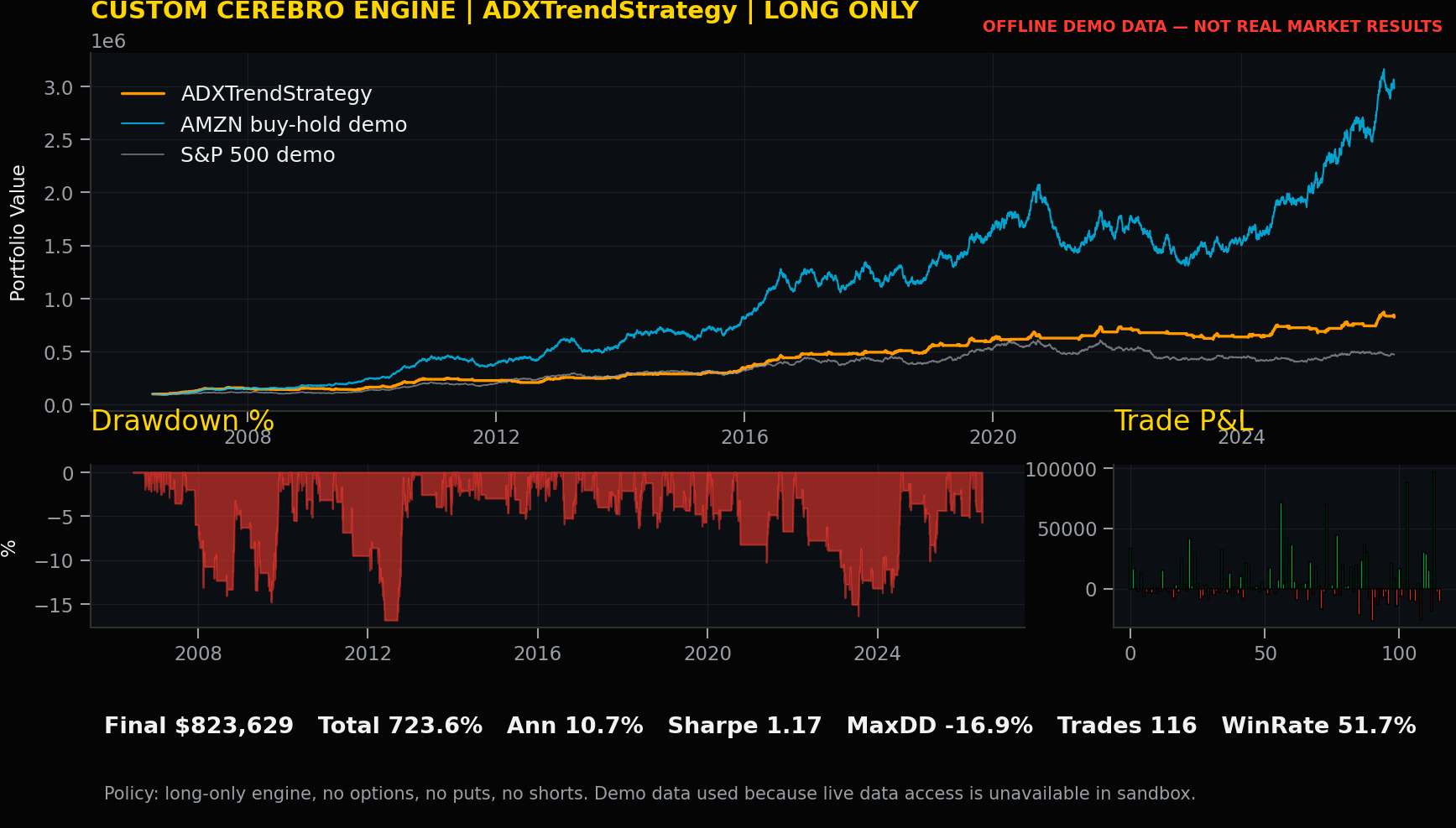

Strategy 15: ADXTrendStrategy

Strategy 15: ADXTrendStrategy

Research purpose. ADX-confirmed trend participation. This strategy is written as a long-only AMZN timing example. It can enter a long position, close a long position, or stay in cash. It does not create short exposure and it does not use options, puts, swaps, futures, margin, or other derivative instruments.

Position-management review. For ADXTrendStrategy, the desk should evaluate whether adx-confirmed trend participation adds useful timing evidence after costs, drawdown, and benchmark context. The review should inspect how often the rule trades, whether exits are understandable, whether the holding period fits the mandate, and whether the signal contributes insight beyond simply holding AMZN through every regime.

Backtrader code. Add this class below the reusable harness, then run run_backtest(ADXTrendStrategy, "ADXTrendStrategy") in a controlled research environment.

class ADXTrendStrategy(TradeLoggerMixin, bt.Strategy):

params = dict(adx_period=14, adx_min=25, ma_period=50, risk_per_trade=0.08)

def __init__(self):

TradeLoggerMixin.__init__(self)

self.adx = bt.ind.ADX(self.data0, period=self.p.adx_period)

self.plus_di = bt.ind.PlusDI(self.data0, period=self.p.adx_period)

self.minus_di = bt.ind.MinusDI(self.data0, period=self.p.adx_period)

self.ma = bt.ind.SMA(self.data0.close, period=self.p.ma_period)

def next(self):

self.risk_exit_check()

if not self.position and self.adx[0] > self.p.adx_min and self.plus_di[0] > self.minus_di[0] and self.data0.close[0] > self.ma[0]:

self.buy_long("adx_positive_trend")

elif self.position and self.plus_di[0] < self.minus_di[0]:

self.close_long("adx_direction_exit")

The agent review for ADXTrendStrategy should summarize the signal path, ledger completeness, risk-control activity, and long-only policy status for this specific strategy run.

Part 9: Executive Committee Summary And Speaking Close

Related summary: Converts the technical research into executive and committee language. This part summarizes what was tested, what remains uncertain, why the workflow does not replace human accountability, and how to speak about results responsibly.

Executive Close And Governance Review

Related summary: Converts the technical workflow into committee language. The section explains how agents accelerate research without replacing accountability, how evidence should be challenged, and how professionals remain responsible for suitability, risk tolerance, data quality, implementation readiness, and final capital decisions.

The close converts benchmark-relative output into decision language. A committee needs to know whether AMZN timing improved relative participation, reduced broad-market drawdown, or simply lowered exposure during difficult periods.

The agent does not replace the professional. Agentic tools can align index data and summarize relative behavior, but benchmark selection, opportunity cost, suitability, and final capital decisions remain human responsibilities.

A disciplined close avoids promotional language. The message is: compare AMZN against its market context, inspect relative strength before claiming skill, and keep accountability with the investment team.

Executive Speaking Close

The final message is benchmark-specific: a profitable AMZN rule still needs to earn its place against Nasdaq, S&P, and Dow context. AgentCore and Strands Agents can organize the comparison, and Backtrader can replay the trades, but the committee must decide whether the relative evidence is useful enough.

Executive Summary For Committee Use

This benchmark-relative article should help reviewers ask whether AMZN strategy behavior was stock-specific, growth-index supported, broad-market dependent, or defensively filtered. The strongest output is not a single winner; it is a clearer map of how each rule behaved against Nasdaq, S&P, and Dow context.

The final decision remains human. Agentic tooling can align benchmarks and summarize relative evidence, but reviewers still need to decide whether the benchmark choice, calendar treatment, and opportunity-cost tradeoff fit the mandate.

Part 10: Sources, Data Notes, And Final Disclosures

Related summary: Keeps sources, data notes, limitations, and final disclosure language together. This part clarifies data assumptions, time windows, AWS design references, and the educational boundary of the article.

Sources And Data Notes

Real-data workflow: executable examples download daily OHLCV data for AMZN, ^NDX, ^GSPC, and ^DJI using yfinance.

Time range: 2006-06-19 to 2026-06-19, subject to market holidays and data-provider availability.

AWS design pattern: Bedrock AgentCore runtime for agent orchestration, Strands Agents for tool coordination, and AWS governed data patterns for lineage, access, and artifact storage.

Education only: not individualized advice, not a solicitation, and not a guarantee of performance.

Final Governance Data Notes

Real-data workflow: executable examples should use approved daily OHLCV data for AMZN, Nasdaq 100, S&P 500, and Dow Jones Industrial Average.

Time range: the example design uses a twenty-year research window and should record exact start and end dates in every run.

AWS design pattern: Bedrock AgentCore runtime can host agent orchestration, while Strands Agents can coordinate tool use and result review.

Education only: not individualized advice, not a solicitation, and not a guarantee of performance.